Introduction

Decentralized finance (DeFi) has been rapidly growing in popularity and has been transforming the financial industry. Furthermore, this growth is bringing up new projects and platforms, each with its own unique tokenomics models.

One such model is the Ve(3,3) tokenomics model, a collaboration between VeChain and 3,3.

In this blog post, we will explore the innovative Ve(3,3) tokenomics model. We will also learn its key features, and how it incentivizes growth and sustainability in the DeFi space. Furthermore, we will discuss the importance of dual token systems, governance incentives, token burns, liquidity rewards, and other factors that contribute to a self-sustaining ecosystem. Join me as I delve into the details of this cutting-edge tokenomics model and discover how it can shape the future of decentralized finance.

What is Tokenomics

Tokenomics is a field that studies the design and economic properties of cryptocurrencies and other blockchain-based digital assets.

It combines principles of economics, game theory, and computer science to analyze the behavior and value of these digital assets.

Tokenomics focuses on how tokens are designed, issued, distributed, and traded within a blockchain network. It also explores the various incentives and mechanisms that drive the behavior of network participants and affect the token’s value.

Tokenomics typically covers a range of topics. It ranges from token supply and demand dynamics, token distribution and allocation, token utility, and governance to token liquidity. There is also the impact of external factors such as regulation and market sentiment.

It is important to note that tokenomics plays an essential role in shaping blockchain-based projects’ success and their tokens. By understanding the economic principles that underlie token design and adoption, developers and investors can make informed decisions that can help drive the growth and sustainability of these emerging ecosystems.

What Is Ve(3,3) Tokenomics Model?

Ve(3,3) is a dual token economic design that allows sustainability. It aims to develop a non-volatile trading environment, different from most single-token economic models.

This model is unique and significant in helping separate the cost of using blockchain from market speculation. Here, incentive and utility are distinct concepts, facilitating upgrades and greater functionalities.

Andre Cronje, the creator of Yearn Finance, originally presented the Ve(3,3) revolutionary decentralized finance (DeFi) tokenomics concept. The concept blends vote escrow tokenomics (“ve”) from protocols like VeChain, Curve, and Convex with the (3,3) design used in the Olympus DAO.

To better understand what ve(3,3) is, let’s first examine the protocol designs for Olympus DAO, VeChain and Curve.

Olympus DAO – “(3,3)”

3,3 decentralized finance (DeFi) platforms aim to provide users with a range of financial services in a decentralized and trustless manner. By leveraging blockchain technology, the 3,3 platform offers a secure, transparent, and efficient environment for users to manage their financial assets, trade cryptocurrencies, and earn rewards.

One of the key features of 3,3 is its dual token system. It consists of a governance token (3C) and a utility token (3CT). This allows for greater flexibility and functionality within the platform. Therefore, users can use 3CT to pay for transaction fees and access platform features. Meanwhile, 3C functions as a voting tool on proposals and decisions related to the platform’s development.

With its unique tokenomics model and commitment to decentralization, 3,3 is well-positioned to play a significant role in the ongoing growth and development of the DeFi ecosystem.

Olympus DAO’s Model Development

Olympus DAO is believed to be the frontrunner in the development of this model, which allows interactions through bonding and staking operations (which are both beneficial for the protocol), and they can also engage in selling operations (which are not beneficial).

Bonding is the practice of swapping tokens (such as DAI or Uniswap LP tokens) for OHM tokens that are locked (staked) for a set amount of time (one-week minimum), at a discounted price.

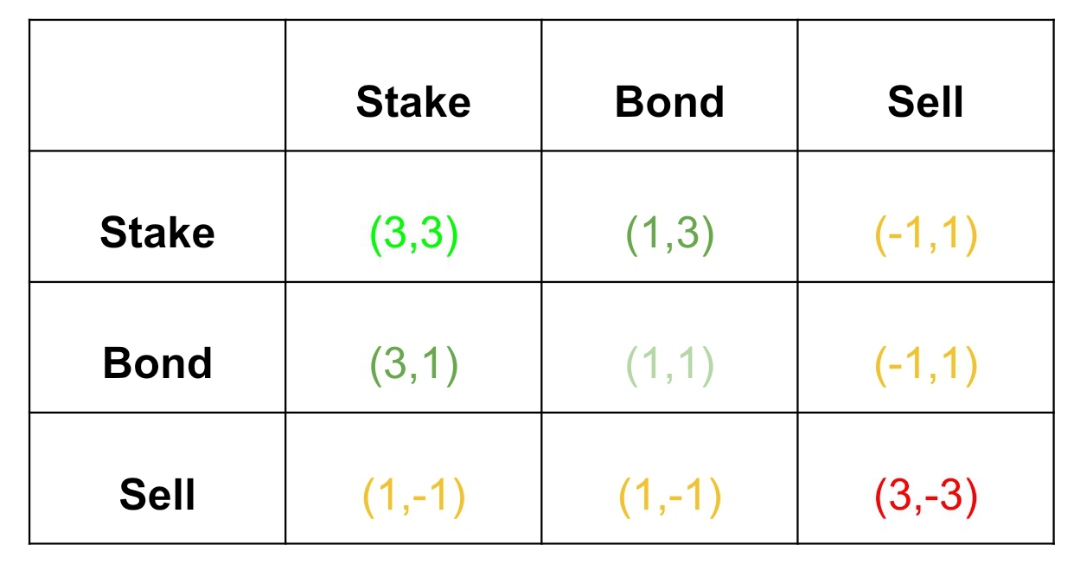

When a 3,3 model is applied, it will result in the following set of outcomes for users. Consider this table from Mettalex

- If both stake (3, 3), it is the best action for both users and the protocol (3 + 3 = 6).

- If one stake and the other one bonds, it is also great because staking takes OHM off the market and puts it into the protocol, while bonding provides liquidity for the treasury (3 + 1 = 4).

- When one of the users sells, it diminishes the effort of the other one who stakes or bonds (1 – 1 = 0).

- When both users sell, it creates the worst outcome for both agents and the protocol (-3 – 3 = -6).

VeChain – “Ve”

Vote escrowed tokens, often known as veTokens, are a common tokenomics paradigm in DeFi. It has been shown to align the incentives of token holders and liquidity providers, leading, among other things, to market outperformance of projects using “VeNomics”.

VeChain (VET) is a blockchain platform that uses a unique tokenomics model to incentivize its users and drive the adoption of its network.

VeChain has a sustainable two-token economic model (VET and VTHO) which is designed to develop a non-volatile trading environment, different from most single-token economic models, where the vechain governance mechanism also serves to stabilize token costs.

This model is unique and significant in helping separate the cost of using blockchain from market speculation. Here, incentive and utility are distinct concepts, facilitating upgrades and greater functionalities. It facilitates enterprise adoption and generates user acceptance.

Features of Vechain “Ve” Tokenomics

Here are some key features of VeChain’s tokenomics model:

- Dual token system: VeChain uses two tokens – VET and VTHO. VET is the main token used for transactions and governance on the VeChainThor blockchain, while VTHO is the energy token used to pay for transaction fees and smart contract execution.

- VeChain Authority Masternodes (VAM): A group of 101 Authority Masternodes secures the VeChain network. They are responsible for validating transactions and ensuring the network’s integrity. To become an Authority Masternode, users must hold a minimum of 25 million VET tokens.

- VeChain Foundation node: The VeChain Foundation operates a node on the network that holds a significant portion of the VET supply. This node is used to fund development initiatives and provide liquidity for the VET token.

- Economic nodes: VeChain also allows users to operate Economic Nodes, which can earn VTHO by staking VET tokens. Economic Nodes are categorized into four levels, each with different requirements and rewards.

- Token burn: A portion of the VTHO that transactions on the network generate will buy back and burn VET tokens, reducing the total supply of VET over time.

Overall, VeChain’s tokenomics model aims to create a self-sustaining ecosystem where users receive incentives to participate in the network and contribute to its growth. The use of dual tokens, Authority Masternodes, and Economic Nodes help to distribute power and rewards across the network, while the token burn mechanism helps to maintain the scarcity and value of the VET token.

Curve Finance – “Ve”

In “ve”, users’ funds (usually the project’s token, e.g CRV) are locked. This grants voting rights, rewards from trading fees, and other benefits (the veTokens, for example, veCRV).

The locking period is usually between a week and four years. The longer the lock, the higher the rewards and voting power.

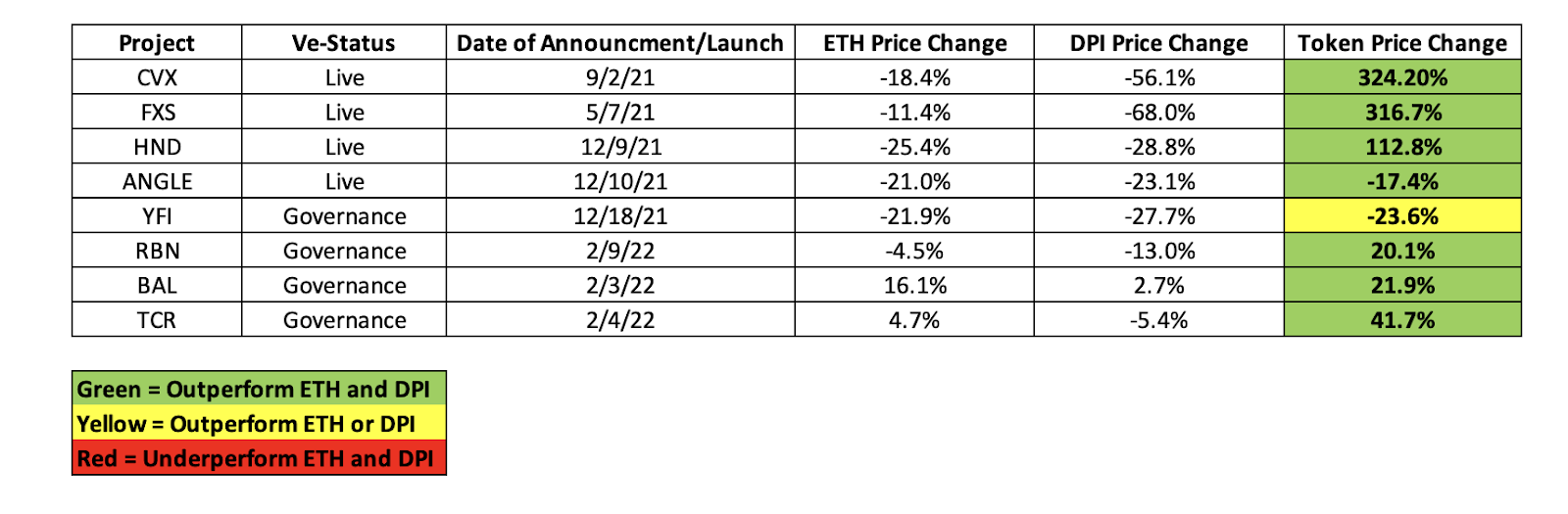

Let’s take a look at this chart from bankless.

It describes the performance of each token against Ethereum(ETH) and DeFi Pulse Index(DPI). You can identify the performance as represented in the “green-yellow-red” chart below the table above.

DPI is a market-wide index that measures the capitalization-weighted performance of decentralized financial assets.

It’s important to note that Curve‘s CRV tokens are governance tokens. Their function is to incentivize liquidity provision on Curve and to involve more users in the governance mechanism.

When users stake CRV, they get a vote escrow token, veCRV. This veToken grants the right to vote, boost users’ CRV rewards and receive trading fees generated from Curve pools. veCRV is basically the governance token for Curve Finance.

There’s a current competition on Curve, “Curve Wars”, where existing protocols compete for a higher voting power, which enables them to select CRV token emission’s direction towards liquidity pools. Liquidity providers (LPs) in a liquidity pool gain more benefits by rerouting CRV token emissions there. This draws more LPs, increasing the liquidity in such pools.

Curve Finance has a “vote locking” innovation, which distributes vote weights and share of rewards proportionately, according to the locking period (one-week minimum). As a result, time-locking a token strengthens its long-term commitment from its holders, decreases its supply in circulation, and alleviates any potential price pressure. Considering staking operations on Curve, it is noticeable that 50% of all trading fees are distributed to veCRV holders.

The Ve(3,3)

Just as the model identifies, it combines the features of both the “Ve” & “(3,3)” models.

The Ve(3,3) design tries to combine these two potent tokenomics approaches to overcome the problems with liquidity mining and the liquidity bootstrapping method used by most DeFi projects that caused the DeFi bubble (and fall) in 2020 – 2021.

Ve(3,3) system rewards active user participation through voting, bribes, and decisions to lock or unlock the governance token.

According to Bankless, “As we know, much of DeFi’s growth over the past year and a half runs on the fuel of liquidity mining. While it often appears at the product level, such as with a DEX or money market, many protocols have also liquidity incentives for their native token through token emissions. While it’s important for a token to have deep liquidity, these programs often go to the extreme to attract yield farmers, resulting in inflation rates that would make Jay Powell blush, and lead to perpetual sell-pressure on the underlying token.

“It doesn’t take a Ph.D. in economics to see why DeFi tokens would underperform: They have a massively inflating supply with no demand to help offset this”.

According to Mettalex, “The goal of ve(3,3) is to better align emission of tokens to beneficial actions and solve the problem with current AMM designs where they subsidize liquidity provision temporarily during fees generation, the more sustainable incentives-generating mechanism, is not”.

Potential Modifications for AMM

A look at Cronje’s Medium Articles suggests that “current AMMs need a few modifications to make it easy for protocols to leverage them:

- Must be able to easily add token incentives to your liquidity.

- Must be able to easily bribe token emissions onto your liquidity.

- Must be able to accrue fees from the liquidity you incentivize.

- Must be able to permissionless deploy your liquidity.”

About ve(3,3) model, Cronje’s Medium Post suggests it will introduce a new AMM with the following features:

- Natively supports swaps between closely correlated assets via a new curve (stable swaps)

- Natively supports swaps between uncorrelated assets

- 0.01% fee

- Fees are paid out in base assets, not converted

- Uniswap v2 compatible interfaces (which allows for support for all existing analytics tools and interfaces)

- Permissionless creation of pools

- Permissionless support for Gauges & BribesEmission incentivizes fees instead of liquidity

- Native support for adding third-party tokens and incentives

- ve(3,3) lockers accumulate all fees for pools they vote emission on

- ve(3,3) lockers increase holdings proportional to emission, with no dilution

- ve(3,3) lockers vote on emissions with circulating supply decay, read more

- ve(3,3) natively supports delegation

- ve(3,3) locks are represented as non-fungible tokens to allow capital efficiency of locks

- No DAO

Ve(3,3) Example – Solidly

To better show how ve(3,3) will work, Cronje implemented the model into his project, Solidly.

Solidly is a DEX on Fantom that enables low-cost, nearly slippage-free trading on assets with weak or strong correlations. Solidly incentivizes fee, not liquidity. This is perhaps the most important innovation of DeFi.

Solidly uses the dual token system which aids users to interact effectively with the protocol, which includes:

- a standard ERC-20 token (i.e. base token) named SOLID, which is also the platform governance token that users can trade in the exchanges.

- ve(3,3) token that is an NFT – veSOLID that is also tradable.

Users need to stake the SOLID tokens to get ve(3,3) NFT tokens – veSOLID.

VeSOLID has a modification to Curve‘s veCRV that allows holders to receive fees from the entire protocol, as it allows users to earn fees from the liquidity pools(also known as GAUGES).

VeSOLID holders also enjoy SOLID emissions based on the circulating supply.

Ve(3,3) Example – Liquify Network

Liquify Network is a DEX on CoreDAO that offers low fees using a governance model called the ve(3,3) system. It is a fork of Solidly.

As a ve(3,3)nomics DEX, it has a dual token system, which includes LIQ and veLIQ. VeLIQ enables voting on the protocol.

VeLIQ is the heartbeat of Liquify Network. Users who lock their LIQ get veLIQ. This enables voting for gauges/pools on a weekly basis, 50% of the trading fees (maybe increase overtime) reward, & 100% of the bribes for the associated pool.

As a permissionless protocol, Liquify Network allows projects to whitelist their tokens. However, the whitelist wallet must hold 0.5% of the total circulating supply of LIQ. Meanwhile, VeLIQ holders can downvote any project with unethical practices like whitelisting fake tokens.

As veLIQ tokens are tradable, a different user from the one who provided liquidity in the first place can hold them to benefit. If this user is a protocol (e.g. Exorde), it could try to attract (or “bribe”) more veLIQ-generated voting power to direct LIQ emissions to its own liquidity pool.

There are two sets of fees for trading in LIQUIFY,

- for volatile assets – 0.4% &

- for stable assets – 0.02%.

50% of these fees go to veLIQ holders, while the other 50% is used to buy back LIQ.

LIQ has no maximum supply limit. However, emissions are distributed in a system of decreasing inflation, resulting in a smaller amount of LIQ tokens being minted over time.

Also, higher veLIQ holdings mean fewer LIQ mint.

Features of Ve(3,3) Tokenomics

Here are some key features of the Ve(3,3) tokenomics model:

- Dual token system: Ve(3,3) uses two tokens – VET and 3CT. VET is the main token for transactions and governance on the VeChainThor blockchain, while 3CT is the utility token transaction fees payment and access platform features on 3,3.

- Economic nodes: Ve(3,3) allows users to operate Economic Nodes, which can earn VTHO by staking VET tokens. In addition, Economic Nodes that also hold 3CT can earn additional rewards in 3CT tokens.

- Governance incentives: Ve(3,3) incentivizes users to participate in the governance process by offering rewards in 3CT tokens for voting on proposals and decisions related to the platform’s development.

- Token burn: A portion of the transaction fees paid in 3CT is used to buy back and burn VET and 3CT tokens, reducing the total supply of both tokens over time. This helps to maintain the scarcity and value of the VET and 3CT tokens.

- Liquidity rewards: Ve(3,3) also incentivizes users to provide liquidity to the VET-3CT liquidity pool by offering rewards in 3CT tokens. The amount of rewards earned is proportional to the amount of liquidity provided and the duration of the liquidity provision.

The Ve(3,3) tokenomics model aims to create a self-sustaining ecosystem. It incentivizes users to participate in both the VeChain and 3,3 networks and contributes to their growth. Furthermore, the use of dual tokens, Economic Nodes, governance incentives, token burn, and liquidity rewards help to distribute power and rewards across the network while maintaining the scarcity and value of the VET and 3CT tokens.

Conclusion

In conclusion, Ve(3,3) is a unique economic design that addresses the issue of volatility in the trading environment. It provides a sustainable solution by utilizing a dual-token system, which allows for more stable and reliable trading. Furthermore, this model is distinct from other single-token economic models and presents an innovative approach to economic design. By mitigating the risks associated with market fluctuations, Ve(3,3) has the potential to revolutionize the trading industry and bring about a more stable and secure economic future.

Personal Note From MEXC Team

Check out our MEXC trading page and find out what we have to offer! You can learn more about crypto industry news. There are also a ton of interesting articles to get you up to speed with the crypto world. Lastly, join our MEXC Creators project and share your opinion about everything crypto! Happy trading!

Join MEXC and Start Trading Today!

{kind=link}