Block Masonry Academy

Author: Won Cha

Recently, on March 10th, the Bitcoin price fell below the 20K mark. One of the possible reasons might be the bankruptcy of Silicon Valley Bank (SVB). This event occurred shortly after the collapse of the 20K mark following the voluntary liquidation of Silvergate Bank. There is also a series of unfortunate events that ensued following SVB’s announcement of a recapitalization (issuing new stocks). This ultimately caused Bitcoin and Ethereum prices to drop by 7% within 12 hours. Examining some key events. First, there was a decline in the leveraged liquidation of Huobi Token. There is also the labeling of Ethereum as a security, the vulnerability of Hedera (Layer 1 Mainnet), and the mention of tax regulation by Biden for cryptocurrency mining. Finally, the closure of Silvergate from regulatory investigations.

In this article, we will first examine why SVB, which has been operating for 40 years, suddenly went bankrupt. We will also see how this is related to the cryptocurrency market, and what possible impact it could have.

What is The Reason for SVB’s Bankruptcy

SVB’s bankruptcy can be attributed to a number of factors. This includes tightening government regulations on cryptocurrency-related activities, leading to difficulties for SVB to operate its banking services. Additionally, the bankruptcy of SVB may have a negative impact on the cryptocurrency market. It serves as a significant institution for providing banking services to cryptocurrency-friendly companies. As such, the cryptocurrency market may experience a short-term decline in investor confidence and overall stability.

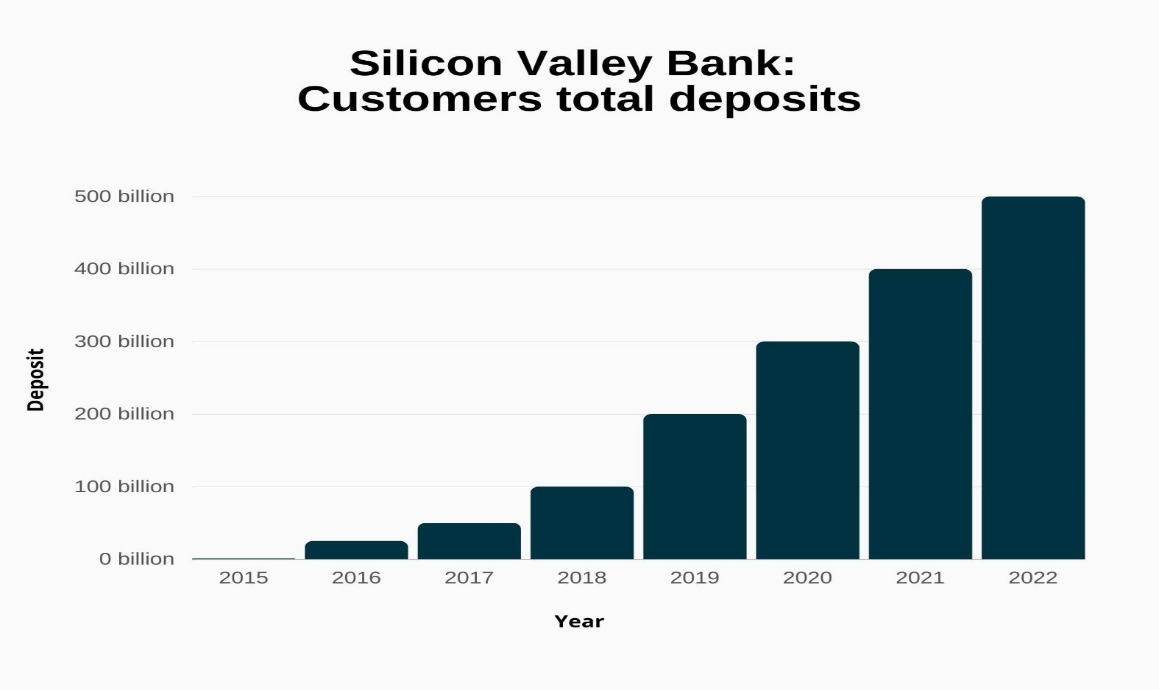

First, let’s examine why SVB Financial decided to sell its available-for-sale (AFS) securities and ultimately went bankrupt about 14 hours after attempting a bank run. Founded in 1983, SVB played a crucial role in funding many startups in Silicon Valley. Normally, traditional banks were hesitant to lend to startups due to their limited assets. To solve this issue for startups, SVB introduced a venture debt product specializing in venture loans. This helped many startups overcome liquidity issues. As a result, SVB had deep relationships with over 50% of VCs in Silicon Valley. They also had 44% of all Tech and Health care companies in the United States as its clients. As of the end of last year, SVB’s total deposits amounted to $175.4 billion, making it the 16th largest bank in the United States by assets.

According to the graph above, SVB Financial Group was experiencing tremendous growth in terms of deposit size when looking at the total deposits increased over the years. To understand the exact cause of the rapid collapse of a bank that was experiencing such rapid growth, it would be helpful to look into SVB’s asset structure closely.

SVB’s Asset Structure

SVB Financial Group had deposits of $173.1 billion. They also held securities worth $91.3 billion as held-to-maturity (HTM) assets and AFS securities of $22.1 billion. HTM securities are those held until maturity. Therefore, it is not recorded on the financial statements, even if their market value falls. This is because the interest payments (coupon) due on the bond are added to the principal until maturity, and the bank receives the full principal plus interest at that time. However, the problem here is that, from the bank’s perspective, deposits are considered liabilities because if customers wish to withdraw, the bank must sell its assets to provide the funds to customers. Therefore, the problem with SVB was that they had too many HTM securities. In the case of SVB, their held-to-maturity securities were predominantly high-quality U.S. 10-year treasury bonds.

Bond prices are inversely related to interest rates, as rising bond yields mean that bond prices have fallen. The interest rate in the U.S. has been constantly increasing. Meaning, the securities held by SVB were incurring losses on their financial statements. As the losses on the securities continued to mount, the ongoing withdrawals by customers caused the losses to accumulate, leading Moody’s to warn SVB that it would have to lower its credit rating due to the constant drop in the value of its held securities.

Failure in Proper Planning

SVB, in consultation with management, planned over the weekend to increase the value of its holdings and adopted the opinion of selling low-yield bonds worth more than $20 billion and reinvesting in more profitable assets. As previously mentioned, the bonds that were previously recorded as unrealized losses on the financial statements became realized losses with the sale, so SVB announces a loss of $1.8 billion. However, to prevent an immediate credit rating downgrade, some of these decisions had to be made.

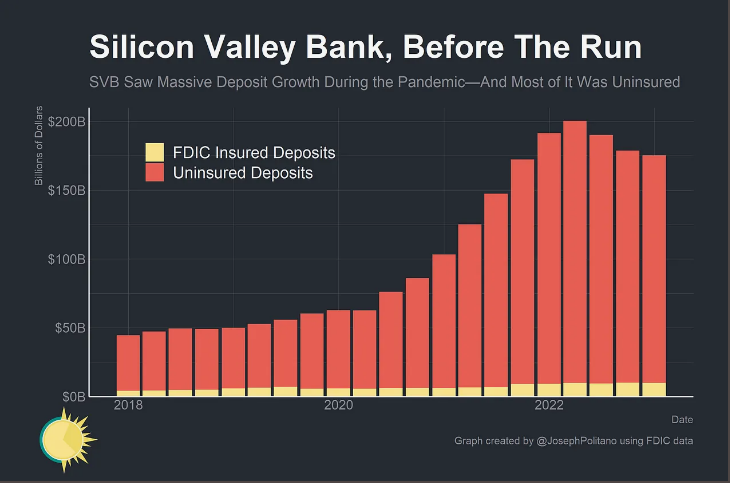

SVB subsequently announced the issuance of $2.25 billion in new shares. However, this announcement actually created negative rumors in the market. Announcing the loss created anxiety and fear among SVB customers. They worry that they might not be able to withdraw their deposits later, and withdrawal requests increased. See the graph below to look at the ratio of Insured & Uninsured deposits to understand why customers of SVB would attempt to withdraw their deposits in such a short period of time.

SVB’s customers were not ordinary people. Instead, they were startups or startup investors living in an environment where they have high exposure to the internet. This creates fear through various SNS, leading to an attempt to withdraw approximately $42 billion, or one-third of the bank’s total deposits, in just one day.

US Teasury’s Intervention

The US financial authorities consequently close SVB on the 10th of March and initiated the process of asset sales by appointing FDIC as the bankruptcy trustee. I would like to express this situation as the “beginning of an excessive simplification of claims”. In the low-interest rate environment, an unexpected interest rate hike by the Federal Reserve and a drop in the price of the debt they held resulted in unrealized losses. Additionally, the financial structure became impaired due to a rush of deposit withdrawals, and a bank run seems to have been attempted.

Some people are comparing the SVB bankruptcy to the Lehman crisis. However, I think it is fundamentally different and is not a systemic risk. For bankrupt Lehman Brothers, they were holding worthless bonds such as junk bonds. Meanwhile, SVB held very high-quality assets, specifically U.S. 10-year Treasury bonds. Thus, the problem was an asset maturity mismatch rather than a fundamental problem. The bank’s customer base is also relevant. Immediate customer withdrawals created a liquidity problem. Personally, I think that this problem could have been resolved if only the liquidity supply issue had been addressed, and stability could have been restored.

After the bankruptcy of SVB, the US Federal Reserve launched a $25 billion bank funding program to prevent bank failures caused by a lack of liquidity. This move is aimed at preventing systemic risks to the banking system due to the bankruptcies and closures of Silvergate, SVB, and New York Signature Bank caused by liquidity shortages. The Fed stated that it will provide one-year loans to eligible banks within the $25 billion limit through this program. This will become an additional source of liquidity for sound securities and will relieve pressure to sell securities due to liquidity constraints.

SVB Bankruptcy in Relation to The Crypto Market

Let’s explore the situations related to the crypto market. First, with the bankruptcy of SVB, the stablecoin USDC suffered direct damage because the reserve fund of USDC, amounting to 3.3 billion, became inaccessible. This amount represents about 8% of the total reserve fund deposited by Circle, the company that issued USDC. As a result of SVB’s inability to withdraw deposits, USDC holders became anxious, and de-pegging occurred.

The incident caused the value of the stablecoin, which is supposed to be pegged at a 1:1 ratio with the US dollar, to drop to $0.88. Users who experienced the collapse of the Terra stablecoin last May would have been more anxious, as they had become worthless despite some users’ initial opinions that it would recover its pegging. Many people would have attempted a bank run. In the case of stablecoins, a bank run means burning the token itself. By burning USDC, the supply of the token decreases, and it can recover to $1 to match demand. Unfortunately, customers believed that the banks Circle used, including Silvergate, SVB, and Signature Bank, which have been closed or bankrupt, have made the situation more difficult.

However, on-chain data showed that Circle burned approximately $2.34 billion worth of USDC in one day. It is actually not considered a significant amount, and the incident appears fundamentally different from the UST’s case. Last May, Luna Foundation Guard (LFG) restored UST pegging by sending BTC to the exchange and issuing an unlimited number of LUNA. However, since USDC is a stablecoin supported by traditional US financial institutions, it was less likely to fail systemically than algorithmic stablecoin UST. Currently, USDC has recovered to $1. (16.03.2023)

Recovery of USD Coin

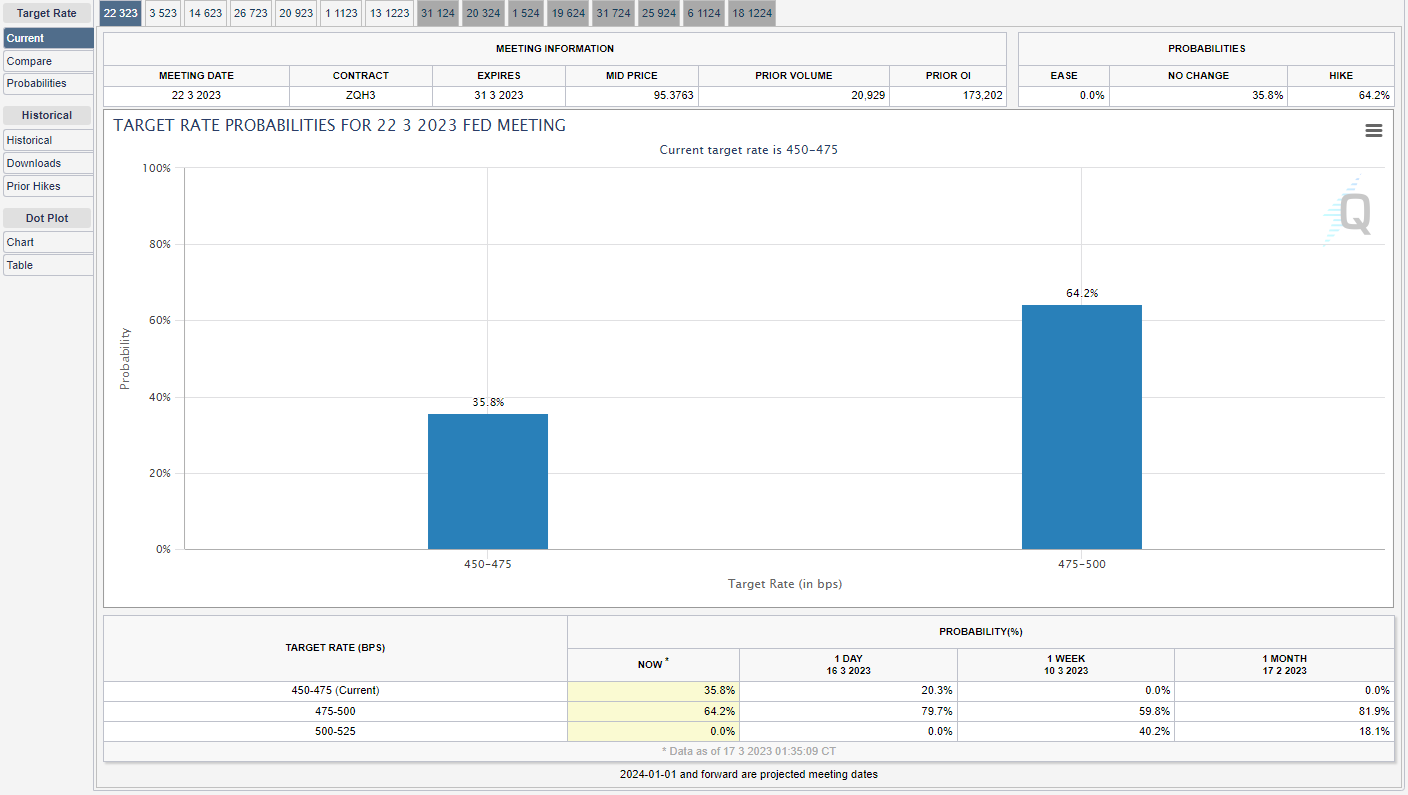

The recovery of USDC played a crucial role in the growth of the crypto market. If USDC had failed to peg, it would have made it difficult for US financial institutions to engage in global finance on public blockchains, potentially preventing the emergence of many web 3.0 products. However, this is not just Circle’s problem. Many crypto firms were also major clients of SVB, such as Pantera Capital, BlockFi, LayerZero, PROOF, a16z, and USV. Personally, I believe that this situation may lead to baby steps by the Fed this month. The probability of a big step is currently 0%. Meanwhile, the probability of a baby step is high at 64.2%. The probability of not raising rates at all is 35.8%, as shown in the graph below.

Despite the optimistic scenario that the Fed did not raise interest rates in a big step, there are concerns about the decrease in cryptocurrency liquidity. This is because banks that play the role of on-ramps have encountered problems at once, leading to a halt in external funds flowing into the crypto market and lowering expectations for the rise of Bitcoin.

Changpeng Zhao, the CEO of Binance, expressed his opinion on Twitter. He mentions that “If regulatory authorities in the United States provide bailout financing to banks in crisis, banks will not feel the need to rigorously manage risk.” He pointed out problems with the existing financial system while emphasizing the importance of the development of the blockchain market. Therefore, I hope that a final lender in the crypto market, similar to the role of the Fed in traditional finance, will emerge so that crypto assets like Bitcoin can be recognized as safe assets.

Personal Note From MEXC Team

Check out our MEXC trading page and find out what we have to offer! You can learn more about crypto industry news. There are also a ton of interesting articles to get you up to speed with the crypto world. Lastly, join our MEXC Creators project and share your opinion about everything crypto! Happy trading!

Join MEXC and Start Trading Today!

{kind=link}