While Amazon (AWS), Microsoft (Azure), and Google Cloud have historically dominated the cloud infrastructure headlines, a massive shift is occurring beneath the surface of the market. Oracle Corporation (ORCL) has quietly positioned itself not just as a competitor, but as the inevitable backbone of the AI era.

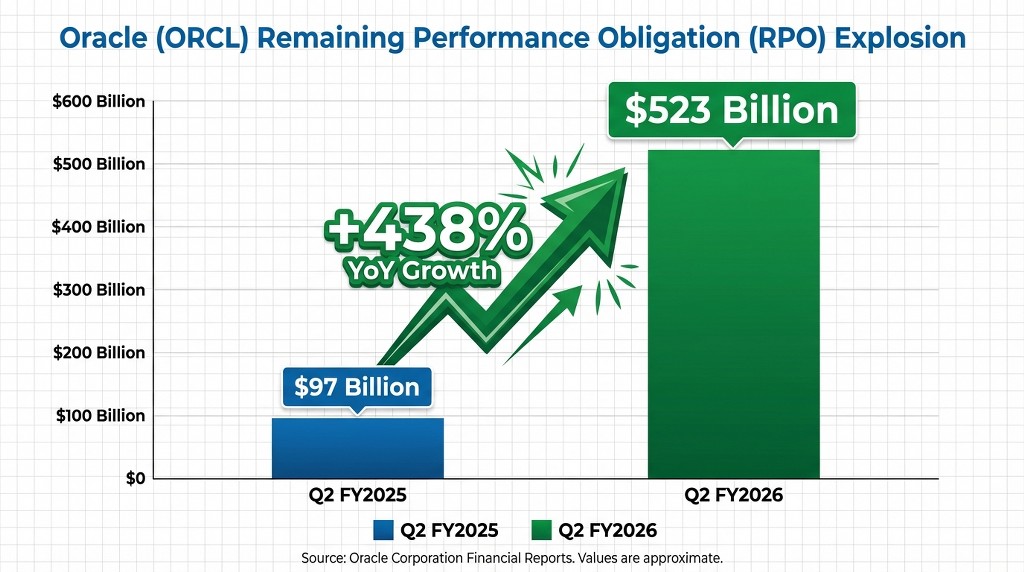

Following the Q2 FY2026 earnings report, Oracle has revealed a statistic that changes the investment thesis entirely: a $523 billion Remaining Performance Obligation (RPO) backlog. This unprecedented figure suggests that while the “Big Three” fight for current market share, Oracle has already secured the future of enterprise AI and cloud workload demand.

Key Takeaways for Investors

- Historic Backlog: Oracle’s RPO surged 438% year-over-year to $523 billion in Q2 FY2026, securing revenue streams for the next decade.

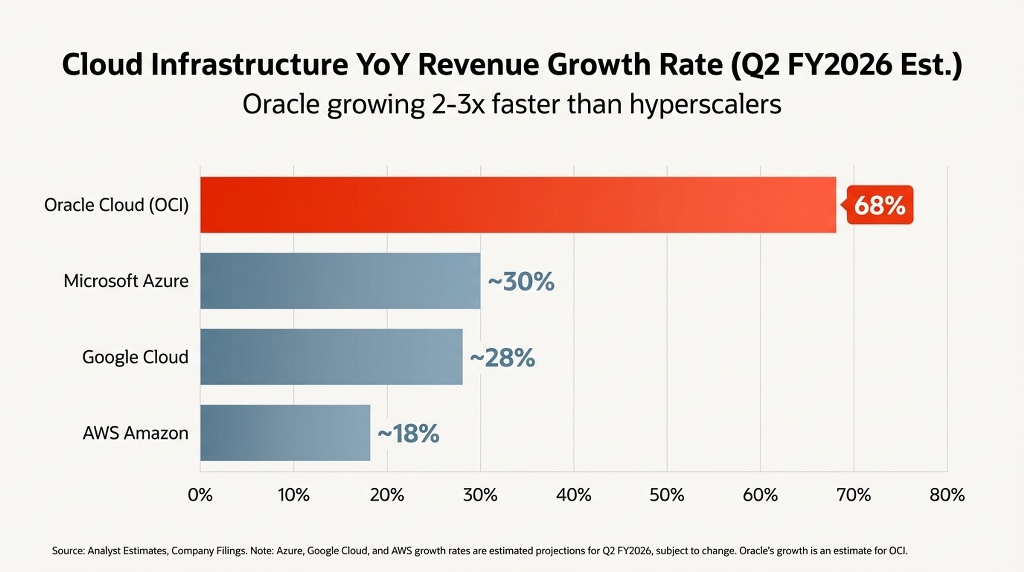

- OCI Hyper-Growth: Oracle Cloud Infrastructure (OCI) revenue grew 68% to $4.1 billion, significantly outpacing the growth rates of AWS and Azure.

- The Multicloud Pivot: Strategic partnerships allow Oracle databases to run inside AWS, Google, and Azure data centers, fueling an 817% spike in multicloud consumption.

- Fiscal Outlook: Management targets $144 billion in revenue by FY2030, driven by rapid data center expansion and AI demand.

Table of Contents

The $523 Billion Signal: Analyzing Oracle’s RPO Explosion

The most critical metric from Oracle’s Q2 FY2026 performance is not just the immediate revenue, but the pipeline. The company reported a staggering $523 billion in Remaining Performance Obligations (RPO). To put this in perspective, this represents a 438% increase compared to the same period last year.

Why RPO Matters More Than Revenue

For investors, Revenue is a backward-looking metric; RPO is a forward-looking indicator of secured demand. This half-trillion-dollar backlog is largely driven by massive, multi-year AI training contracts with industry leaders like OpenAI, NVIDIA, and Meta.

Unlike volatile spot-market sales, these contracts represent guaranteed future cash flow. Oracle has effectively locked in high-margin infrastructure revenue for years to come, insulating it from short-term economic fluctuations that might affect its competitors.

OCI Performance: Outpacing the Hyperscalers

While Oracle’s total revenue for Q2 FY2026 grew a respectable 14% to $16.1 billion, the real story lies within the Oracle Cloud Infrastructure (OCI) segment.

The 68% Growth Engine

OCI revenue hit $4.1 billion, marking a 68% year-over-year increase. In comparison, market leaders like AWS and Azure are seeing growth rates stabilize in the 15-20% range (AWS) and 30% range (Azure) due to the law of large numbers. Oracle’s ability to sustain near-triple-digit growth suggests it is capturing net-new market share rather than just riding industry tailwinds.

Infrastructure Scale-Out

- Current Footprint: Oracle is rapidly expanding its data center capacity to meet this backlog.

- Expansion Plan: The company is moving from 71 live data centers to a target that supports a $144 billion revenue run-rate by FY2030.

- Efficiency: By utilizing a highly automated “cookie-cutter” data center design, Oracle brings capacity online faster and cheaper than legacy providers.

The Strategic Pivot: “Chip Neutrality” and Multicloud

Oracle’s resurgence is credited to two strategic decisions by Chairman Larry Ellison and CEO Safra Catz: Multicloud Interoperability and Chip Neutrality.

1. The Multicloud Genius

Instead of fighting a losing battle to force customers to move everything to Oracle Cloud, Oracle partnered with its rivals. Through Oracle Database@Azure, OracleDatabase@Google Cloud, and OracleDatabase@AWS, customers can run high-performance Oracle SQL databases directly inside competitor data centers.

- Result: Multicloud consumption skyrocketed 817% in Q2 FY2026.

- Benefit: This creates a “win-win” where Oracle monetizes the database layer regardless of which cloud provider the customer uses for compute.

2. Chip Neutrality

Oracle has moved away from proprietary silicon lock-in. By embracing an open architecture that supports NVIDIA GPUs, AMD chips, and Ampere processors equally, OCI has become the preferred destination for training massive AI models. This flexibility allows customers to avoid vendor lock-in, a major pain point with AWS and Google.

Comparative Analysis: Oracle vs. The Big Three

For investors evaluating the cloud landscape in 2026, the differentiation is clear. Oracle is no longer a legacy software company; it is a specialized high-performance cloud provider.

| Feature | Oracle (OCI) | AWS (Amazon) | Azure (Microsoft) | Google Cloud (GCP) |

| Q2 FY26 Growth | 68% (Infrastructure) | ~17-19% (Est) | ~30% (Est) | ~28% (Est) |

| Primary Strength | Database Speed & Cost | Market Scale & Breadth | Enterprise Integration | AI & Data Analytics |

| Pricing Strategy | Aggressive (Low outbound fees) | Premium Pricing | Bundled Pricing | Competitive |

| Multicloud Stance | Fully Open/Embedded | Walled Garden | Hybrid Focus | Open Source Focus |

Verdict: For generic storage and compute, AWS remains king. However, for mission-critical databases and high-performance AI training, OCI is winning on price/performance ratios.

Valuation & Financial Health

Despite the bullish backlog, investors must weigh the financials objectively.

- Total Revenue: $16.1 Billion (+14% YoY).

- EPS (Non-GAAP): $2.26 (+54% YoY).

- Margins: Operating margins are expanding as the high-capital expenditure phase of the cloud build-out begins to yield recurring revenue.

The “Hockey Stick” Projection

Management has outlined a clear path to $144 billion in revenue by FY2030. With $523 billion already in RPO, this target appears less like an aspiration and more like a mathematical certainty, assuming execution remains stable. The stock currently trades on these future growth expectations, making it a “growth at a reasonable price” (GARP) candidate compared to the lofty valuations of pure-play AI stocks.

Future Outlook and Investment Risks

The Bull Case

- AI Demand: As long as global demand for AI model training exceeds chip supply, OCI’s optimized clusters will be fully booked.

- Sticky Revenue: Database migrations are notoriously difficult. Once a customer optimizes their Oracle Database on OCI, they rarely leave.

The Bear Case (Risks)

- Capital Expenditure (CapEx): Building data centers to fulfill a $523B backlog requires massive upfront cash. Investors should monitor Free Cash Flow (FCF) closely to ensure debt levels remain manageable.

- Execution Risk: rapidly scaling from ~70 to 100+ data centers involves logistical hurdles that could delay revenue recognition.

Market Watch: Capitalizing on the Cloud Wars

Oracle is no longer sleeping; it is aggressively taking market share from the Big Three. For traders, this volatility signals opportunity.

While traditional investors wait for quarterly reports, active traders are already positioning themselves. Whether you are looking to leverage the breakout driven by the 68% OCI growth or short the resistance levels during CapEx cycles, you need a platform that moves as fast as the market.

Why Trade ORCL on MEXC?

- Flexibility: Trade in both directions (Long/Short) with Stock Futures.

- Accessibility: Access high-performance assets seamlessly alongside your crypto portfolio.

Conclusion

Oracle has successfully executed one of the most difficult pivots in tech history: transitioning from a legacy licensing business to a high-growth cloud infrastructure giant. The $523 billion backlog serves as a fortress around its valuation, providing visibility that few other tech companies can match.

For investors looking beyond the hype of the “Magnificent Seven,” ORCL represents a matured, highly profitable cloud play with significant runway for growth in the AI era.

Frequently Asked Questions (FAQ)

- Is Oracle actually beating AWS and Azure?

In terms of total market share, no, AWS and Azure are still larger. However, Oracle is growing significantly faster (68% vs 20-30%) and is winning specific high-value battles in database management and AI training clusters.

- What does the $523 billion backlog mean for ORCL stock?

It means Oracle has contractually secured nearly half a trillion dollars in future revenue. This reduces the downside risk for the stock, as future earnings are less dependent on new sales and more dependent on simply delivering existing contracts.

- Why did ORCL stock fluctuate after the Q2 earnings?

While the backlog was record-breaking, total revenue ($16.1B) slightly missed some aggressive Wall Street whispers. This is typical “growing pains” volatility. Smart money often looks at the backlog (future growth) rather than a minor quarterly revenue miss.

- Is ORCL a good stock for AI exposure?

Yes. Unlike hardware stocks (like NVIDIA) which are cyclical, Oracle provides the infrastructure where AI lives. Its partnerships with OpenAI and xAI position it as a critical utility provider for the AI revolution.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please conduct your own research (DYOR) and assess your risk tolerance before trading. MEXC does not accept liability for any investment decisions made based on the information provided herein.